The rise of one-click stablecoin checkout

Stablecoin payments are transitioning from speculative trading instruments to standard e-commerce infrastructure. In 2026, the friction of traditional cross-border transactions is being replaced by the speed and low cost of blockchain-based settlements. This shift is not about replacing fiat currency but about optimizing the payment rails that move it.

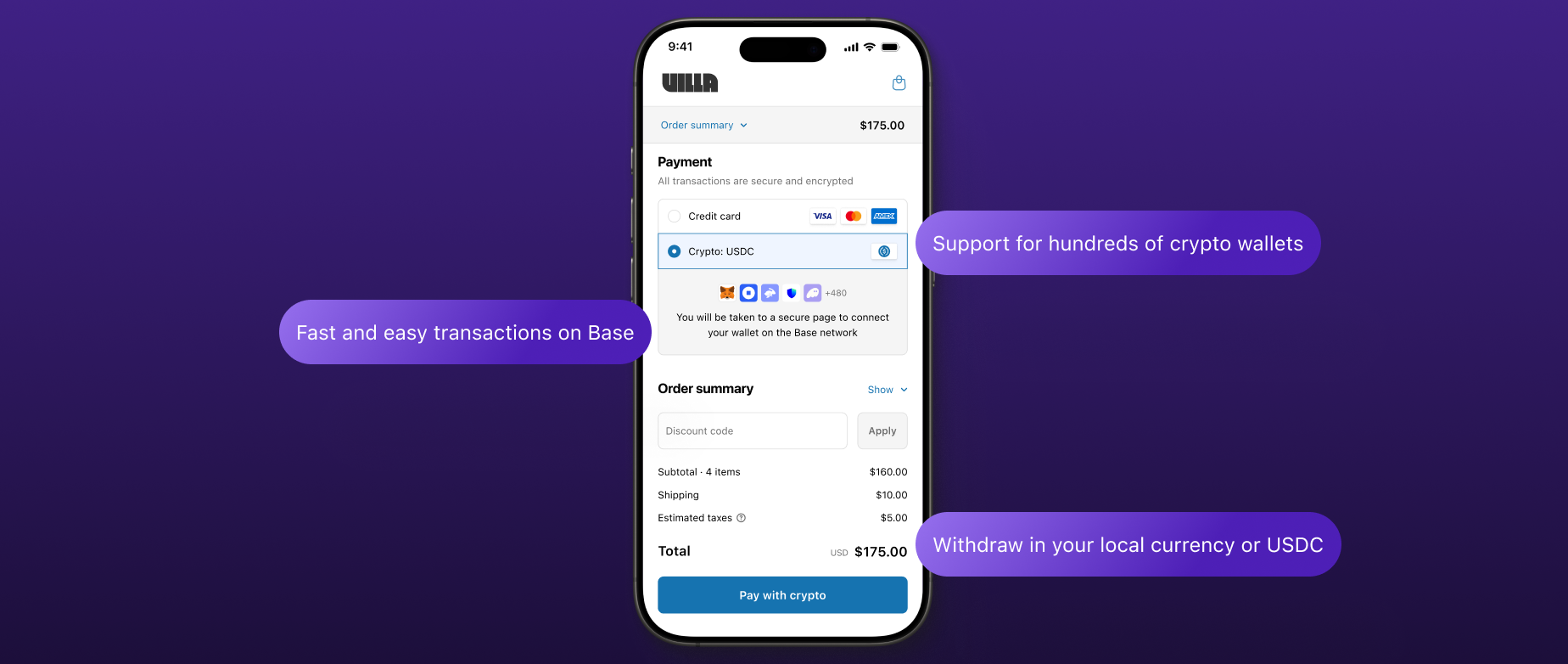

The core advantage lies in the "one-click" experience. By integrating stablecoin payment gateways, merchants can offer consumers a checkout flow that bypasses the multi-day settlement cycles and high interchange fees of credit cards. This is particularly impactful for global commerce, where currency conversion and banking delays often stall sales.

Major payment processors are now enabling this capability for enterprise merchants. As noted by Checkout.com, these integrations allow businesses to accept stablecoin payments directly, giving them more ways to capture global demand without managing complex crypto custody themselves. This institutional adoption signals that stablecoins are becoming a reliable, everyday option for digital commerce.

The stability of the underlying asset is critical. Merchants rely on tokens like USDC, which are pegged to the US dollar and backed by reserves, to avoid the volatility that plagues other cryptocurrencies. This stability ensures that the value received at checkout matches the value settled, making it a viable alternative for risk-averse businesses.

To understand the reliability of this asset class, it helps to look at the price stability of major stablecoins over time.

Chart: USDC/USD price stability on Binance. The tight peg to the dollar demonstrates the low volatility required for merchant acceptance.

This stability, combined with near-instant settlement, creates a compelling case for one-click stablecoin checkout. It reduces chargeback risks, lowers transaction costs, and opens up new markets for merchants willing to adopt this emerging technology.

How the technology bridges Web2 and Web3

One-click stablecoin checkout functions by abstracting the complexity of blockchain transactions into a familiar e-commerce interface. Instead of requiring customers to manage private keys, seed phrases, or gas fees, the system handles the on-chain settlement in the background. This allows merchants to accept digital assets with the same frictionless experience as a credit card transaction, effectively bridging the gap between traditional retail UX and decentralized financial rails.

The mechanism relies on specialized APIs and SDKs that act as intermediaries between the storefront and the blockchain. When a customer selects the stablecoin payment option, the provider’s infrastructure generates a secure transaction request. This can be executed via hosted checkout pages, embedded widgets, or headless integrations, depending on the merchant’s technical setup. Solutions like Crossmint allow users to pay without even possessing a crypto wallet initially, as the provider can facilitate the asset transfer on their behalf before settling the funds to the merchant.

Behind the scenes, these platforms often employ smart routing and multi-currency support to optimize transaction success rates. By intelligently selecting the most efficient blockchain network or stablecoin variant, the system minimizes latency and cost. This technical layer ensures that the merchant receives the agreed-upon value, while the customer experiences a seamless, single-click confirmation. The result is a payment method that retains the speed and stability of fiat currency while leveraging the transparency and programmability of blockchain technology.

Leading crypto payment SDKs for 2026

Use this section to make the One-Click Stablecoin Checkout decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Compliance and risk in stablecoin payments

Integrating stablecoin checkout is not merely a technical upgrade; it is a regulatory undertaking. As financial institutions and merchants adopt these assets, the burden of compliance intensifies. The primary risk lies in the intersection of digital asset volatility and stringent anti-money laundering (AML) frameworks. Unlike traditional fiat rails, stablecoin transactions occur on public ledgers, creating an immutable audit trail that regulators are increasingly scrutinizing.

KYC (Know Your Customer) requirements remain the gatekeeper for adoption. Merchants must ensure their payment processors verify the identity of users to prevent illicit flows. This is where partnerships with established providers become critical. For instance, Checkout.com’s integration with Coinbase allows eligible enterprise merchants to accept stablecoins while leveraging Coinbase’s compliance infrastructure. This model shifts the heavy lifting of regulatory adherence away from the individual merchant and onto specialized financial rails.

The regulatory landscape is fragmented and evolving. What constitutes compliant behavior in one jurisdiction may be prohibited in another. Merchants must navigate local laws regarding digital asset classification, tax reporting, and consumer protection. Relying on unofficial advice or generic crypto forums is dangerous in this high-stakes environment. Guidance must come from official regulatory bodies or primary legal counsel specializing in digital assets.

Failure to align with these standards can result in frozen assets, hefty fines, or the revocation of banking relationships. The "one-click" convenience of stablecoin payments must be built on a foundation of rigorous compliance. As the 2026 e-commerce shift accelerates, those who prioritize regulatory integrity will mitigate risk and build sustainable trust with their customer base.

Integrate one-click stablecoin checkout

Migrating to stablecoin payments requires integrating a provider’s SDK, but the workflow is streamlined through established partnerships. Major processors like Checkout.com now allow eligible merchants to accept USDC directly, settling funds without manual conversion steps. This reduces friction for both the developer and the end user.

Choose a processor that supports stablecoin settlement. Providers like Checkout.com and Crossmint offer APIs that handle the complexity of blockchain transactions, allowing you to accept crypto while settling in fiat or stablecoins.

Register for a merchant account and generate your API keys. Secure these credentials immediately. You will need them to authenticate requests between your e-commerce platform and the payment provider’s gateway.

Before going live, run transactions in the provider’s sandbox. Verify that the one-click flow triggers correctly and that webhooks fire as expected. This step is critical for identifying edge cases in transaction confirmation.

Set up webhook endpoints to listen for payment confirmations on the blockchain. Once verified, switch your API keys to production mode. The one-click experience is now active for your customers.

Frequently asked questions about stablecoin checkout

What is a stablecoin payment method?

Stablecoin payments utilize digital tokens pegged to fiat currencies, such as the US dollar, and backed by corresponding reserves. This structure allows merchants to accept crypto without exposing consumers to the extreme volatility typical of other digital assets. Major payment processors like Checkout.com now enable enterprise merchants to accept these payments directly, bridging traditional e-commerce with digital asset liquidity.

How to withdraw stablecoin?

To withdraw stablecoins, navigate to your platform’s withdrawal page via the web interface or mobile app. Select the stablecoin asset, choose the source account, and specify the destination wallet address. Ensure the receiving wallet supports the specific blockchain network to prevent irreversible loss of funds.

Are stablecoin payments faster than credit cards?

Yes. Stablecoin transactions settle on the blockchain in minutes or seconds, bypassing the multi-day settlement cycles of traditional credit card networks. This speed reduces operational friction and improves cash flow for merchants, particularly for cross-border transactions where traditional banking rails are slow and costly.

No comments yet. Be the first to share your thoughts!