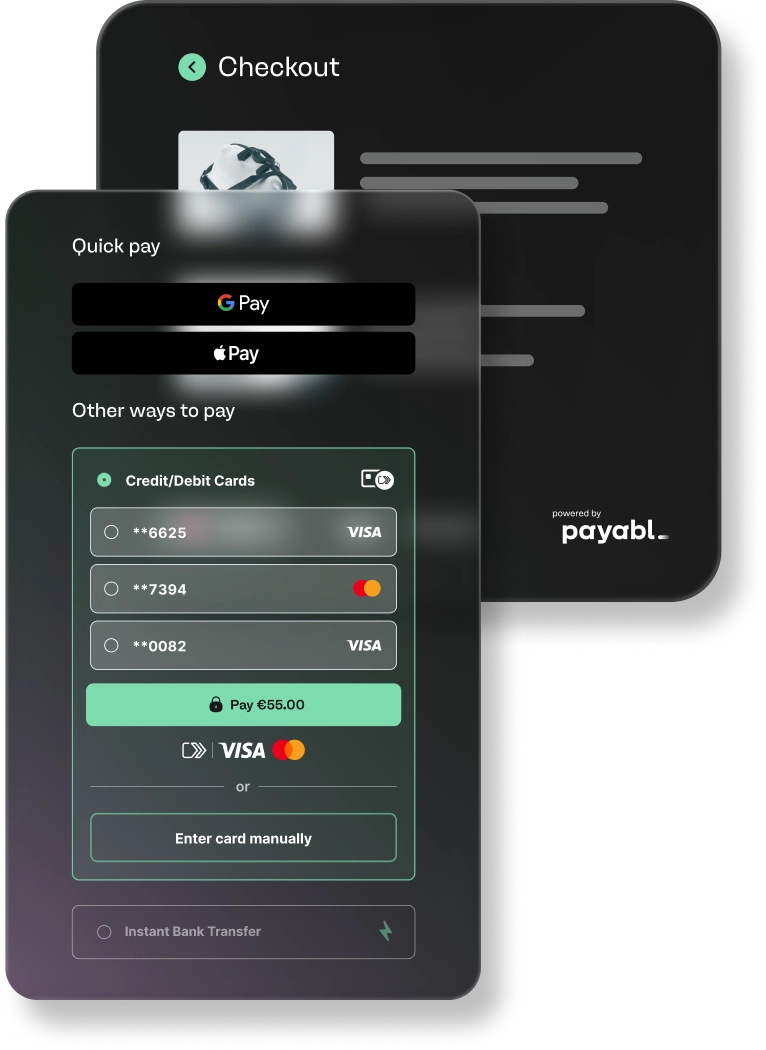

Why merchants need one-click stablecoin checkout

Traditional cross-border payments remain a bottleneck for global commerce. A standard wire transfer often takes three to five business days to settle, tying up working capital and introducing uncertainty for both the buyer and the seller. In contrast, stablecoin transactions settle on-chain in minutes, regardless of weekends or holidays. This speed is not just a convenience; it is a structural advantage for businesses operating across time zones and currencies.

The financial friction of traditional crypto onboarding has historically been a barrier to adoption. Merchants often face complex compliance hurdles, volatile exchange rates, and high processing fees when accepting Bitcoin or Ethereum. One-click stablecoin checkout solves this by decoupling the transaction from volatility. By using a stablecoin pegged to a fiat currency, merchants receive immediate, predictable value without the need for immediate conversion or hedging strategies. This reduces the risk of holding digital assets and simplifies accounting.

The business case extends beyond speed. Stablecoin payments offer transparency and programmability, allowing for automated reconciliation and lower transaction costs compared to international card networks. As noted by Circle, the next phase of digital commerce is defined by these efficiencies, enabling merchants to reach global customers without the friction of currency conversion or delayed settlements.

Top stablecoin payment SDKs for 2026

The landscape for one-click stablecoin checkout is dominated by three providers that handle the complexity of blockchain settlement while keeping the user experience identical to traditional card payments. For merchants, the choice of SDK determines not just which chains are supported, but how quickly funds settle and whether the integration requires significant engineering overhead.

| Provider | Integration Type | Settlement | Target Audience |

|---|---|---|---|

| Checkout.com | Hosted & Embedded | Fiat (USD/EUR) | Enterprise Merchants |

| Crossmint | Hosted, Embedded, Headless | Crypto or Fiat | Web3 Native & Gaming |

| WalletConnect | Embedded (SDK) | Crypto or Fiat | DeFi & Mobile Apps |

Checkout.com leverages its existing fiat infrastructure to allow merchants to accept stablecoins like USDC and USDT, settling immediately into bank accounts. This approach minimizes volatility risk for traditional retailers but requires enterprise-level onboarding. Their SDK is designed for high-volume merchants who need a familiar payment flow without managing private keys.

Crossmint offers a more flexible stack for digital-native businesses. Their SDK supports hosted, embedded, and headless checkout options, making it suitable for gaming platforms and NFT marketplaces that need to onboard users who don’t yet have crypto wallets. The system handles the minting and transfer processes in the background, abstracting away the blockchain complexity entirely.

WalletConnect focuses on embedded experiences for mobile and web applications. By integrating directly into the app’s UI, it allows users to pay with stablecoins using their existing wallets without leaving the application. This is particularly effective for decentralized finance (DeFi) platforms and mobile-first services that prioritize user retention and seamless transitions.

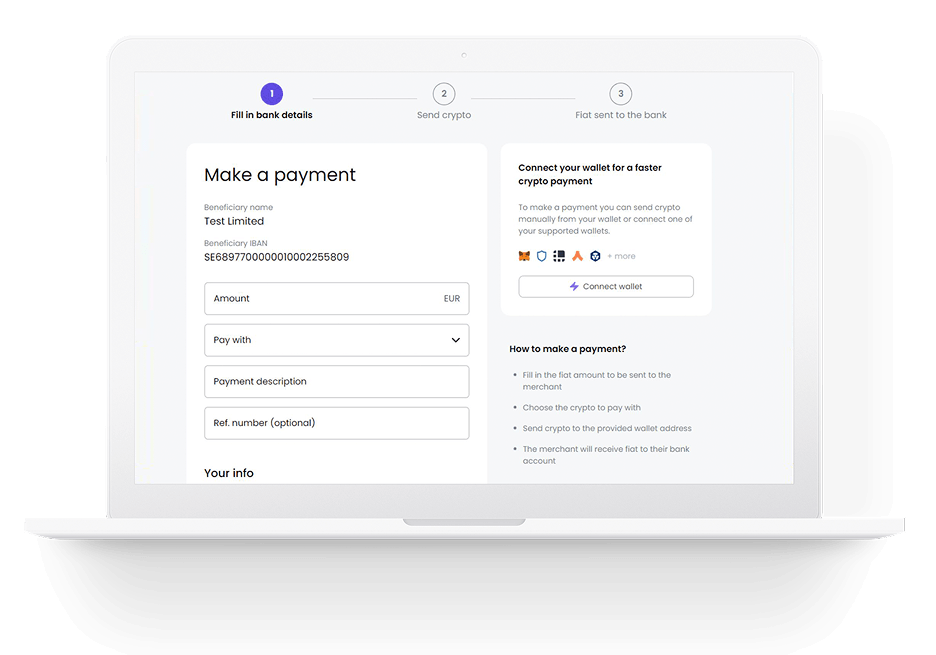

Settlement mechanics and fiat conversion

The primary hurdle for merchants accepting stablecoins is not the transaction speed, but the exposure to volatility and regulatory complexity. Without immediate conversion, a merchant holding USDC or USDT faces the risk that the peg could break or that tax authorities may view the asset as property rather than currency. Modern one-click checkout SDKs solve this by automating the settlement layer, allowing merchants to choose between holding stable assets or receiving instant fiat.

Most enterprise-grade integrations rely on partnerships with specialized crypto infrastructure providers. For example, Checkout.com partnered with Fireblocks to enable USDC settlements, leveraging institutional-grade custody and conversion rails. This approach ensures that the merchant’s balance sheet remains insulated from crypto market swings. The SDK handles the on-chain swap or off-ramp in the background, crediting the merchant’s bank account in USD, EUR, or GBP within the standard settlement window.

This distinction is critical for high-volume retailers. When the SDK auto-converts, the merchant never actually holds the stablecoin; the provider does. This mirrors the traditional acquiring model where the bank takes the risk and settles funds later. By using provider-backed widgets and official partnership details, businesses can integrate stablecoin payments without building a treasury management system from scratch.

Compliance and risk management in SDKs

Integrating stablecoin checkout is not just a technical integration; it is a regulatory undertaking. Modern SDKs are designed to handle the heavy lifting of financial compliance, ensuring that businesses can accept payments without exposing themselves to sanctions violations or money laundering risks. The SDK acts as a gatekeeper, verifying identities and screening transactions against global watchlists before any funds move.

Automated KYC and AML checks

The most critical function of a compliant SDK is the automated execution of Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols. Rather than building these checks from scratch, developers rely on the SDK to interface with licensed verification providers. This includes identity document validation, biometric checks, and real-time sanctions screening against lists maintained by the OFAC, UN, and EU.

By embedding these checks directly into the checkout flow, the SDK ensures that only verified, compliant users can initiate transactions. This reduces the operational burden on the business and minimizes the risk of accidental non-compliance, which can result in severe fines or the revocation of payment licenses.

Regulatory adherence and stability

Stablecoin payments operate in a rapidly evolving regulatory landscape. SDKs must be updated frequently to reflect changes in local laws, such as the EU’s Markets in Crypto-Assets (MiCA) regulation or emerging US state-level guidelines. A robust SDK abstracts these complexities, ensuring that the integration remains compliant as regulations shift.

This adherence extends to the stability of the asset itself. As noted by Visa, programmable stablecoins offer fast, stable, and borderless payments, but this stability relies on the issuer’s reserves and the underlying infrastructure’s integrity. SDKs help mitigate counterparty risk by integrating only with issuers that meet strict regulatory and reserve requirements, protecting the merchant from de-pegging events or issuer insolvency.

Risk mitigation strategies

Beyond compliance, SDKs provide tools for real-time risk management. These include transaction monitoring, velocity checks, and fraud detection algorithms that analyze patterns to flag suspicious activity. By leveraging these built-in features, businesses can maintain a low-risk profile while offering the speed and efficiency that stablecoins provide.

The integration of these risk management tools is essential for any business looking to scale stablecoin payments. It ensures that the checkout experience is not only fast and seamless but also secure and compliant with the highest standards of financial regulation.

Integration steps for one-click checkout

Integrating one-click stablecoin checkout requires connecting your platform to a payment processor’s API. The goal is to abstract blockchain complexity so users pay with familiar fiat methods while you receive stablecoins. This guide walks through the technical workflow for embedding these components securely.

Begin by registering for a merchant account with a provider like Crossmint or Stripe. Obtain your sandbox API keys from the developer dashboard. These keys allow you to test transactions without moving real funds. Configure your environment variables to store these keys securely, never hardcoding them in client-side code.

Access the provider’s developer portal to create a new application. Generate a publishable key for the frontend and a secret key for your backend server. Ensure you select the correct network (e.g., Ethereum, Solana) for the stablecoin you intend to accept.

Integrate the provider’s SDK into your frontend. Most providers offer a hosted checkout or an embedded widget that handles wallet connections and fiat on-ramps. Use the publishable key to initialize the component. This approach reduces liability, as the provider handles sensitive payment data and compliance checks.

Import the SDK into your React or Vue application. Render the checkout button or modal using the provided component wrapper. Pass configuration options such as currency pairs (e.g., USD to USDC) and allowed networks. Ensure the component responds to user clicks by triggering the payment flow.

Set up a webhook endpoint on your backend to receive real-time transaction updates. The provider will POST events to this URL when a payment is initiated, confirmed, or failed. Verify the webhook signature using your secret key to prevent spoofing. Update your order status in your database only after receiving a "confirmed" event.

Create an endpoint (e.g., /api/webhooks/stablecoin) that listens for POST requests. Parse the payload to extract the transaction ID and status. If the status is "confirmed," mark the order as paid. If it is "failed" or "expired," notify the user and allow them to retry.

Before going live, run end-to-end tests in the sandbox environment. Use test cards or simulated wallet addresses to trigger payments. Verify that webhooks fire correctly and that your database updates match the provider’s status. Check edge cases, such as network congestion or user abandonment, to ensure your UI handles errors gracefully.

Simulate a full user journey from checkout initiation to payment confirmation. Use the provider’s sandbox tools to generate test transactions. Confirm that your webhook handler processes the final "confirmed" event and updates your internal ledger. Once verified, switch your API keys to the live environment.

Stablecoin market outlook

One-click stablecoin checkout is moving from experimental to standard infrastructure as digital commerce scales. The growth is driven by speed, transparency, and the ability to reach global markets without traditional banking friction. Major issuers are positioning stablecoins as the next phase of digital payment rails.

Institutional interest is accelerating this transition. As payment processors and fintech platforms integrate these tools, the barrier to entry for cross-border transactions continues to drop. This shift signals a broader acceptance of programmable money in everyday commerce.

Frequently asked questions about stablecoin checkout

Stablecoin integration simplifies global payments, but merchants and developers still face specific operational and technical questions. The following answers address common concerns regarding liquidity, cash-outs, and lending risks based on current market data and official guidelines.

No comments yet. Be the first to share your thoughts!