Why one-click stablecoin checkout matters now

One-click stablecoin checkout replaces the friction of traditional payment gateways with instant, on-chain settlement. For merchants, this shift is not just about adopting new technology; it is about reclaiming control over capital flow. Traditional credit card processing involves a complex web of intermediaries—issuing banks, acquiring banks, and card networks—that collectively delay funds and extract significant fees. Stablecoin payments bypass this legacy infrastructure, allowing value to move directly from buyer to seller.

The business case rests on three pillars: speed, cost reduction, and transparency. Unlike fiat transfers that can take days to clear, stablecoin transactions settle in seconds or minutes, regardless of the time of day or geographic location. This immediacy improves cash flow management and reduces the risk of chargebacks, a persistent headache for online retailers. The programmability of stablecoins also enables automated reconciliation and smart contract-driven escrow, features that are difficult and expensive to implement with legacy banking systems.

The cost disparity is stark. While traditional gateways often charge between 1.5% and 3.5% per transaction plus fixed fees, stablecoin networks typically charge fractions of a cent. This efficiency is particularly critical for high-volume or low-margin businesses. As major issuers like Circle expand their infrastructure, the reliability and liquidity of stablecoin payments continue to improve, making them a viable primary payment method rather than a niche alternative.

How one-click stablecoin checkout works

The one-click stablecoin checkout process bridges the gap between consumer crypto assets and merchant fiat settlement. It removes the friction of manual wallet transfers by automating the connection, conversion, and settlement layers. When a shopper selects a crypto payment option, the integrated SDK handles the complex backend logic, allowing the transaction to complete in seconds rather than minutes.

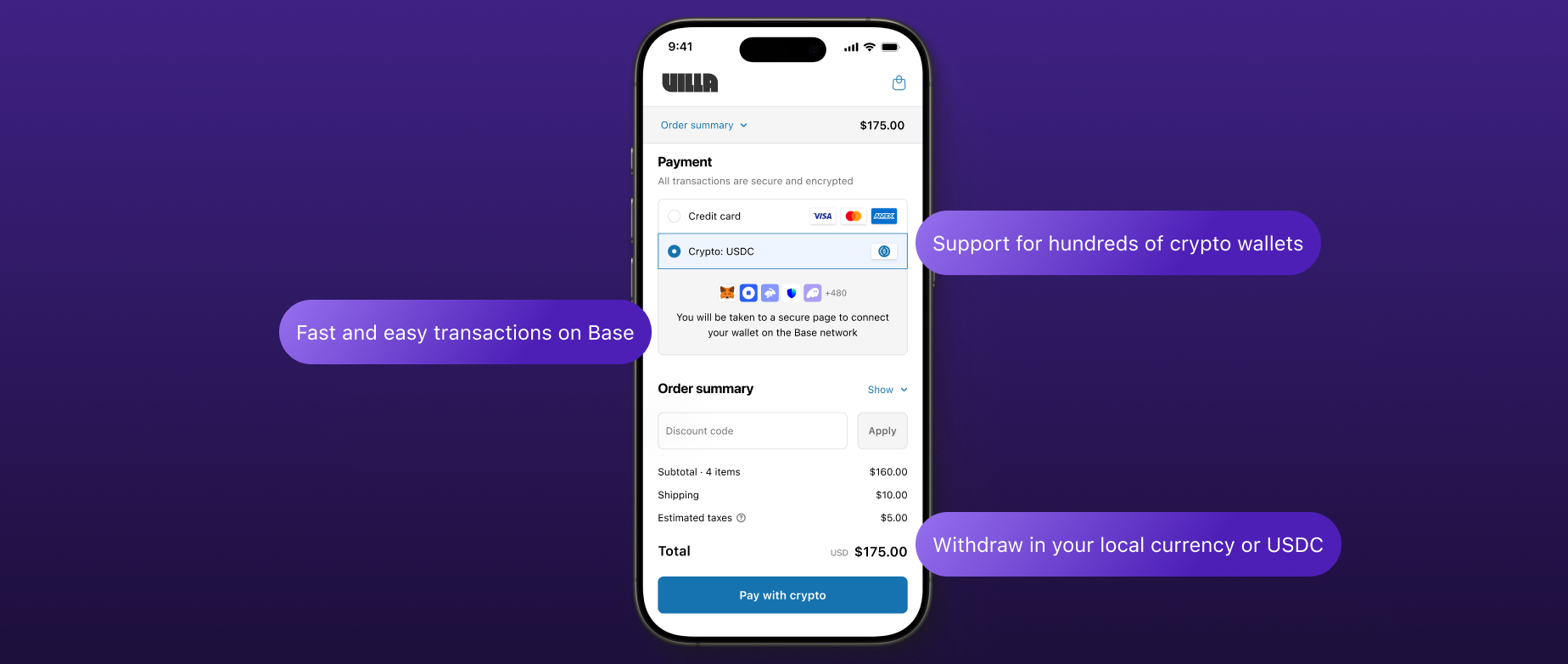

1. User selects crypto and connects wallet

The checkout flow begins when the customer chooses a stablecoin payment method, such as USDC or USDT. The merchant’s integrated SDK prompts the user to connect their digital wallet (like MetaMask or Coinbase Wallet) or select a card-to-crypto conversion option. This step verifies the user’s identity and available balance without requiring them to leave the checkout page. The SDK ensures the selected stablecoin is compatible with the merchant’s preferred settlement network.

2. SDK handles conversion and routing

Once the wallet is connected, the SDK initiates the transaction. If the merchant prefers fiat settlement, the SDK automatically routes the stablecoin through a payment processor or decentralized exchange to convert it into USD or EUR. This conversion happens in real-time, locking in the exchange rate to protect both the buyer and seller from volatility. The SDK manages the gas fees and network selection, often choosing the most cost-effective blockchain, such as Polygon or Solana, to ensure speed and low costs.

3. Settlement occurs on-chain

The final step is the on-chain settlement. The stablecoin transfer is broadcast to the blockchain network and confirmed within seconds. For merchants using fiat settlement, the processor receives the stablecoin, converts it, and deposits the fiat currency into the merchant’s bank account, typically within 24 hours. For merchants holding crypto, the stablecoin lands directly in their treasury wallet. This immutable record provides instant proof of payment, reducing chargeback risks and reconciliation errors.

The checkout flow begins when the customer chooses a stablecoin payment method. The merchant’s integrated SDK prompts the user to connect their digital wallet or select a card-to-crypto conversion option. This step verifies the user’s identity and available balance without requiring them to leave the checkout page.

Once the wallet is connected, the SDK initiates the transaction. If the merchant prefers fiat settlement, the SDK automatically routes the stablecoin through a payment processor to convert it into USD or EUR. This conversion happens in real-time, locking in the exchange rate to protect both the buyer and seller from volatility.

The final step is the on-chain settlement. The stablecoin transfer is broadcast to the blockchain network and confirmed within seconds. For merchants using fiat settlement, the processor receives the stablecoin, converts it, and deposits the fiat currency into the merchant’s bank account. This immutable record provides instant proof of payment.

Top stablecoin checkout SDKs for 2026

Integrating one-click stablecoin checkout requires choosing an SDK that balances developer speed with financial reliability. The market has consolidated around providers that abstract the complexity of wallet creation and transaction routing. Below is a comparison of the leading options for 2026, evaluated on integration ease, supported chains, and fiat off-ramp capabilities.

| Provider | Supported Chains | Integration Type | Fiat Off-Ramp |

|---|---|---|---|

| Crossmint | EVM, Solana | Hosted, Embedded, Headless | Via partners |

| TransFi | Multi-chain | One-click SDK | Smart routing |

| Checkout.com | EVM (USDC) | API-first | Fireblocks settlement |

| Polygon Pay | Polygon | Wallet abstraction | Native bridge |

Crossmint

Crossmint focuses on removing friction for non-crypto-native users. Their Digital Asset Checkout API allows merchants to accept digital assets without requiring the customer to hold a wallet first. This "no-wallet-needed" approach significantly increases conversion rates by treating crypto payments like standard credit card transactions. They support hosted, embedded, and headless integrations, making them flexible for various tech stacks. While they support multiple chains including EVM and Solana, fiat settlement is handled through partner networks rather than direct bank integrations.

TransFi

TransFi offers a one-click integration designed specifically for e-commerce stores. Their solution emphasizes AI-powered smart routing to ensure the lowest fees and fastest transaction times across multiple currencies. By supporting a wide range of stablecoins, TransFi allows merchants to accept payments in the currency most convenient for their global customer base. The SDK handles the complex routing logic, ensuring that transactions are settled efficiently. Fiat off-ramping is managed through their smart routing infrastructure, which can direct funds to preferred liquidity providers.

Checkout.com

Checkout.com brings enterprise-grade reliability to stablecoin payments. Their integration with Fireblocks allows merchants to settle payments in USDC directly. This option is ideal for businesses that already use Checkout.com for traditional payments, as it unifies crypto and fiat flows under a single dashboard. The integration is API-first, requiring more development effort than hosted solutions but offering greater control over the user experience. Fiat settlement is robust, leveraging Fireblocks' security infrastructure to ensure compliance and safety.

Polygon Pay

Polygon Pay leverages the Polygon network to provide low-cost, fast stablecoin transactions. Their SDK includes wallet abstraction features, allowing users to pay with stablecoins without managing private keys directly. This is particularly effective for merchants targeting users on the Polygon network, where gas fees are negligible. The native bridge capabilities allow for seamless conversion between stablecoins and fiat, though the ecosystem is more focused on Polygon-specific integrations compared to multi-chain competitors.

Integrating the SDK into your checkout flow

Building a one-click stablecoin checkout requires balancing speed with security. The integration path typically splits into two distinct approaches: hosted checkouts for rapid deployment and embedded SDKs for full brand control. Both methods abstract the complex blockchain interactions, allowing your platform to accept payments in seconds rather than minutes.

Hosted checkout solutions, such as those offered by Crossmint, allow users to pay with credit cards or existing crypto wallets without leaving your site. This approach minimizes development overhead and reduces the risk of user error during the transaction process. It is ideal for merchants prioritizing time-to-market over deep UI customization. For teams needing granular control over the user experience, embedded SDKs provide the necessary hooks to integrate wallet abstraction directly into your existing interface.

Regardless of the method chosen, the settlement layer remains critical. Polygon’s payment infrastructure, for instance, enables stablecoin transactions to clear in approximately five seconds with negligible fees. This speed is essential for maintaining the frictionless experience that defines one-click commerce. By leveraging these established protocols, you ensure that the backend settlement is as seamless as the frontend interaction.

Managing risk and compliance in stablecoin payments

One-click stablecoin checkout offers speed and transparency, but it operates in a regulatory environment that is still maturing. Unlike traditional card networks, stablecoin transactions are irreversible. This permanence eliminates chargeback fraud but shifts the burden of verification entirely onto the merchant and the payment processor. To operate legally in 2026, businesses must implement robust Know Your Customer (KYC) and Anti-Money Laundering (AML) checks that satisfy both local financial authorities and blockchain analytics standards.

Stablecoins themselves are generally pegged to fiat currencies, but they are not risk-free assets. Regulatory scrutiny focuses on the reserves backing these tokens. Merchants should prioritize processors that only support fully reserved, audited stablecoins like USDC or USDT to minimize counterparty risk. The Circle blog notes that the next phase of digital commerce relies on this trust infrastructure. Without it, a "one-click" experience could quickly become a liability if the underlying asset depegs or faces regulatory bans.

Compliance also requires monitoring transaction patterns. Because blockchain ledgers are public, every payment is traceable. Integrating real-time screening tools ensures that funds do not originate from sanctioned addresses or mixers. This is not just a legal requirement; it protects your business from being flagged by banking partners who may still hold your fiat settlement accounts. Treating stablecoin payments as a high-risk financial channel rather than a simple e-commerce feature is essential for long-term stability.

Frequently asked questions about stablecoin checkout

Stablecoins maintain their value by being pegged to reserve assets, typically government bonds or cash equivalents. This stability allows merchants to accept payments without the extreme volatility seen in Bitcoin or Ethereum. For real-time market data on major stablecoins, refer to the live price widget above.

No comments yet. Be the first to share your thoughts!